Latam VC Report 2026: Exits Surge and Stronger VC Ecosystems in Chile, Uruguay and Brazil

Latam VC Report 2026 reveals a rebound in venture capital investment, rising exits and a shift toward larger rounds and fewer startups.

The Latam VC Report 2026 reveals that venture capital investment in Latin America is recovering, but with a clear shift toward larger rounds and fewer startups receiving funding. According to the report, produced by Cuantico VP in collaboration with Startuplinks, US$4.126 billion was invested across 681 venture capital deals in 2025, reflecting a 13.8% increase in deployed capital compared to 2024.

Despite the rebound, the ecosystem has entered a more disciplined phase often described as “more money for fewer startups.” Investors are deploying capital more selectively, focusing on stronger companies, clearer paths to exits and more sustainable valuations. At the same time, Chile, Uruguay and Brazil are emerging as the most efficient venture capital ecosystems in the region, while exits activity is gaining momentum.

Investors show cautious optimism but remain focused on exits

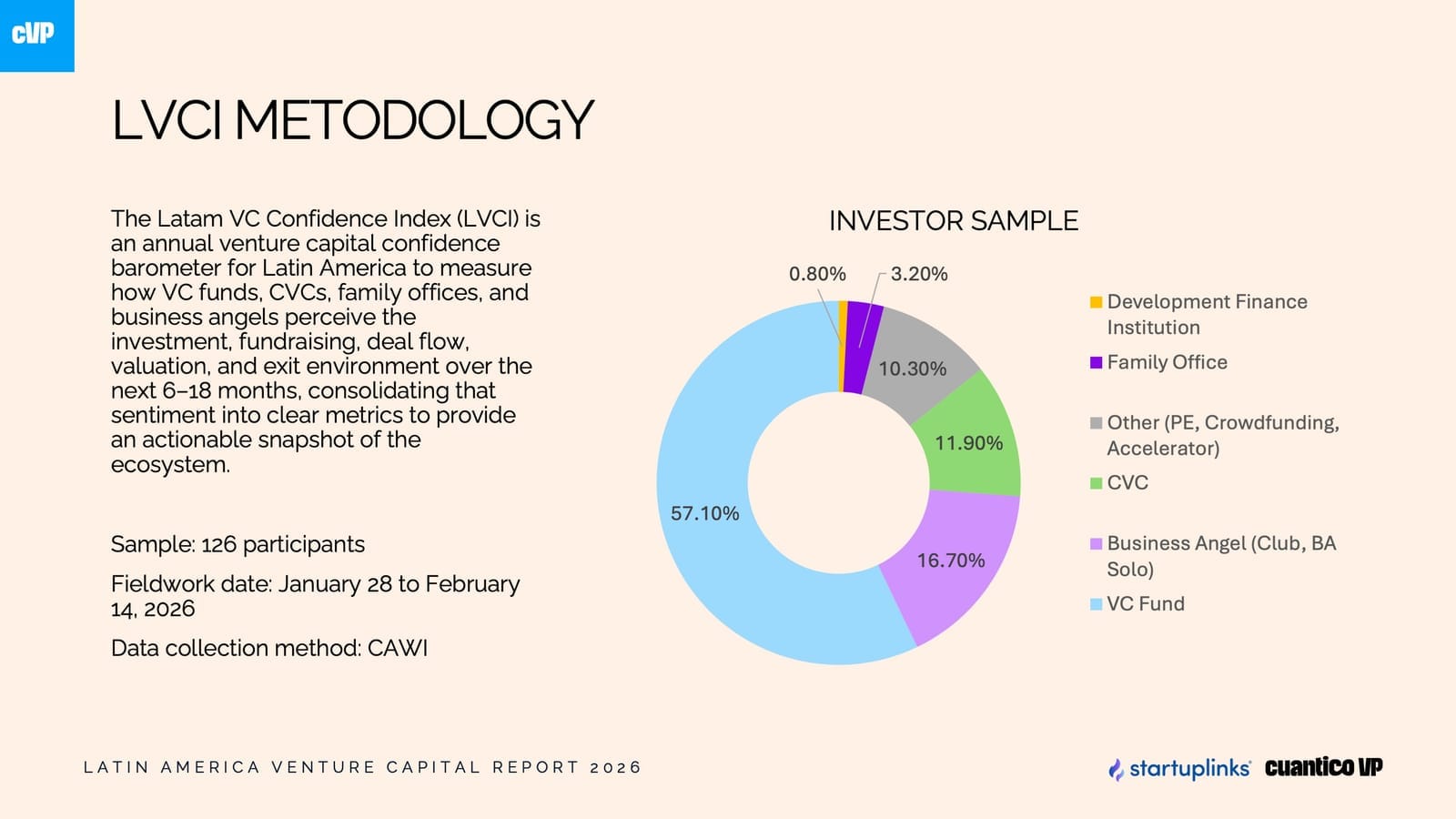

The Latam VC Confidence Index (LVCI), based on responses from more than 100 investors including VC funds, angel investors, corporate venture capital firms and family offices, suggests the market is approaching a turning point.

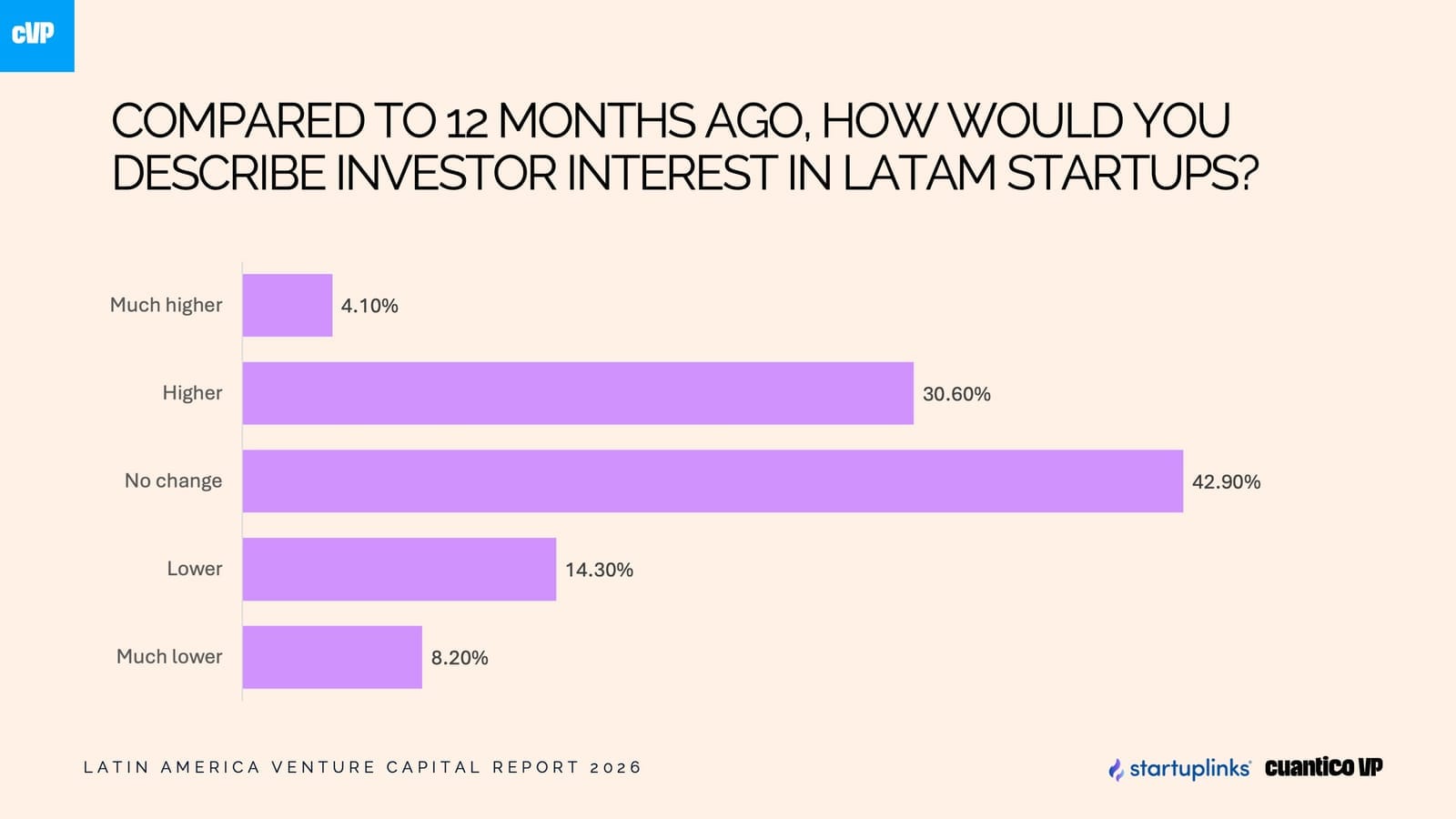

About 58% of investors report medium-to-high confidence for the next six to eighteen months, while 47.2% plan to increase investment activity in 2026. Another 7.2% expect a significant increase in deployments.

However, fundraising conditions remain uncertain. Nearly 49.2% of respondents consider the fundraising environment neutral compared with last year, and only 6.4% expect a clear improvement.

Startup valuations also show diverging perceptions across the ecosystem:

- 37.3% of investors believe valuations are fair

- 36.5% consider them overvalued

- 21.4% see them as undervalued

Liquidity continues to be one of the main concerns. 62.7% of investors view the exits environment as unfavorable, citing limited exit opportunities (73.8%), political instability (57.1%), and reduced participation from limited partners (44.4%) as the main risks for 2026.

“Investing in Latin America is relatively cheaper, but capital has learned it cannot ignore political context or the quality of returns,” Jose Kont, Executive Director of Cuantico VP.

Founders face longer fundraising cycles but remain optimistic

From the founders’ perspective, the Startuplinks Confidence Index captures the views of 49 startup founders who have already raised venture capital, including companies at pre-seed (55%), seed (33%) and Series A (12%) stages.

More than 53% of founders describe the fundraising environment as unfavorable or very unfavorable, reflecting the increased selectivity among investors.

Fundraising cycles have also lengthened. Around 30.6% of founders are still in the process of closing their funding round, while 24.5% of those who completed one took between six and twelve months to secure capital.

Even so, founder confidence remains strong:

- 53.1% say they are very optimistic about their company’s growth

- 51% expect to raise a new round within the next 12 months

Their main concerns mirror those of investors, particularly limited exit opportunities (49%), low participation from local institutional investors (46.9%), and political instability (38.8%).

“Capital exists, but reaching it now requires more traction, more time and a stronger narrative,” said Israel García Ballesteros, CEO of Startuplinks.

Startup exits in Latin America reach US$4.9 billion

One of the most notable findings in the Latam VC Report 2026 is the rebound in startup exits across the region.

In 2025, venture-backed exits reached US$4.9 billion, representing a 172% increase compared with US$1.8 billion in 2024. The number of deals remained almost unchanged at 63 transactions, meaning the average exit size tripled.

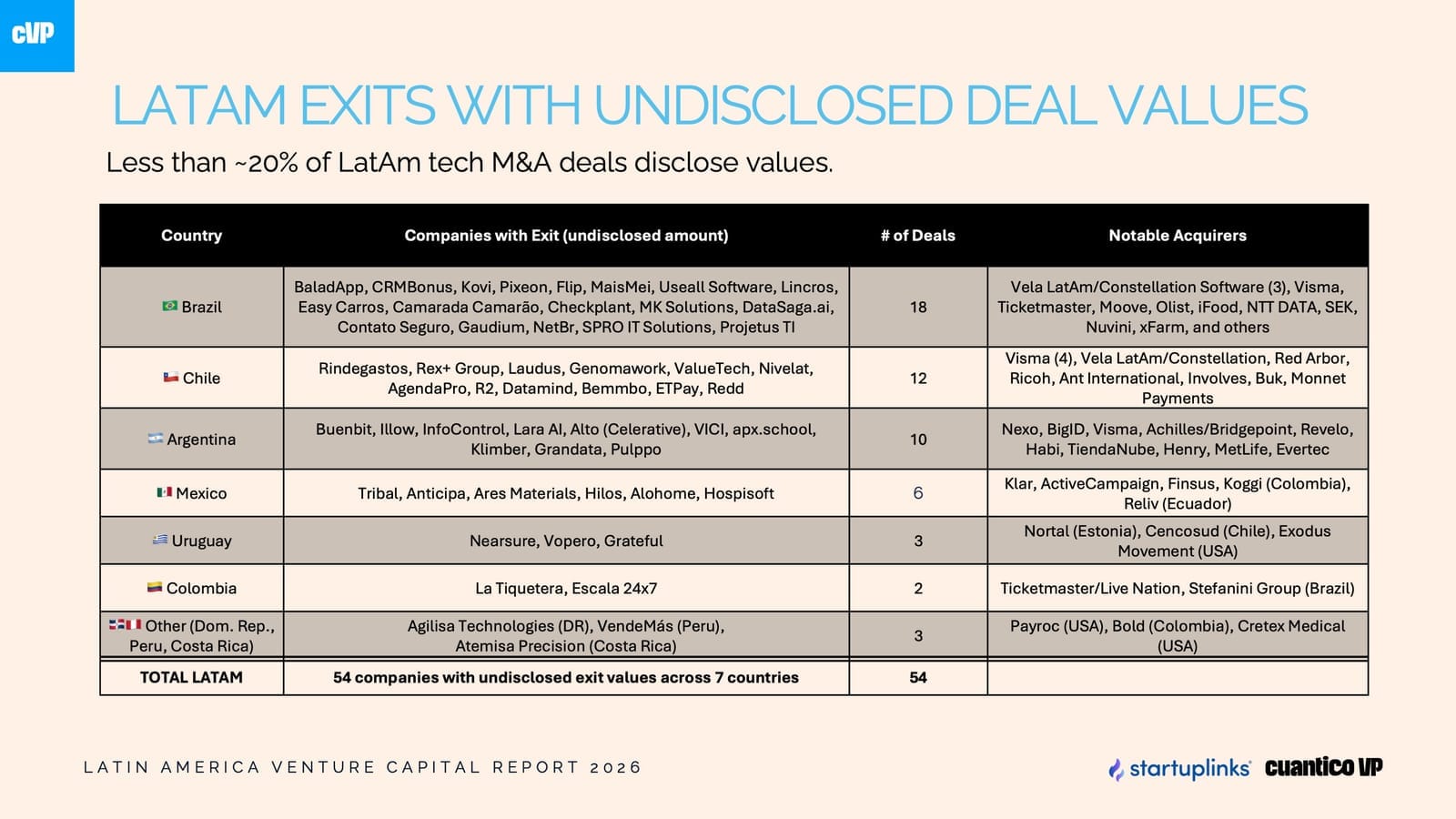

When the broader private equity and growth capital ecosystem is considered, the report identifies US$6.1 billion in liquidity across 15 disclosed transactions, plus 55 additional deals without public values. This suggests the real size of the exits market could be up to four times larger than what is publicly visible.

Mergers and acquisitions dominate the landscape, accounting for 67% of exits, followed by secondary transactions (27%).

Two transactions concentrated nearly half of the value among the largest exits:

- Prosus’ US$1.7 billion acquisition of Despegar

- Securitize’s US$1.25 billion SPAC listing

Meanwhile, companies such as Vercel, Plata, Contabilizei and Omie illustrate how secondary liquidity during growth rounds is becoming increasingly common in the region.

“The lack of liquidity in Latin America often acts as a mechanism that protects long-term value against public market volatility,” Kont noted.

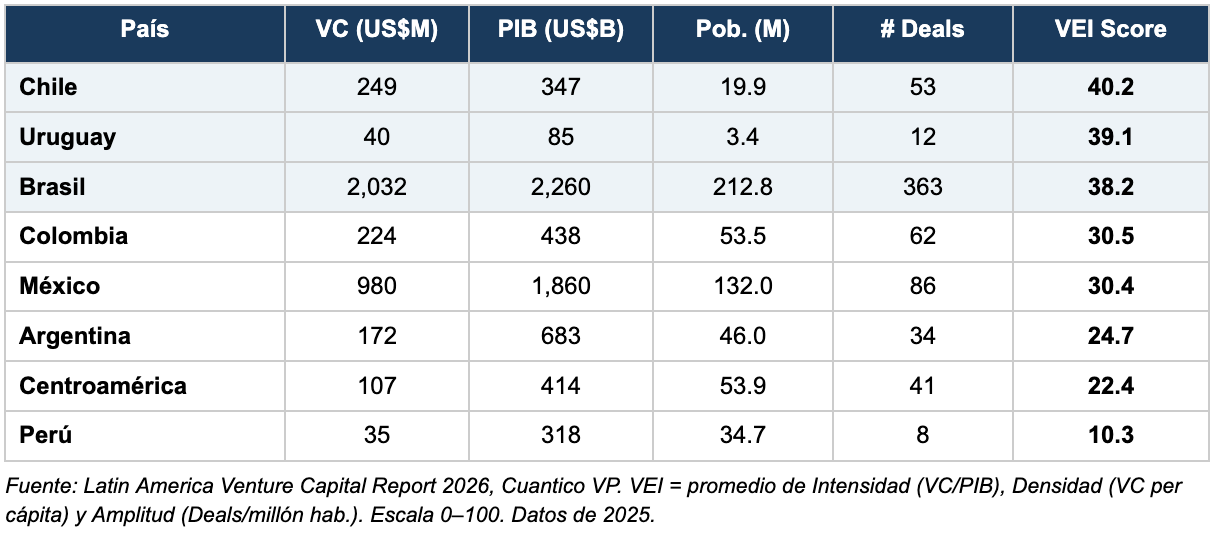

Chile, Uruguay and Brazil lead venture capital ecosystem efficiency

The report also introduces the VC Efficiency Index (VEI), a metric designed to measure the strength of venture capital ecosystems based on three indicators:

- VC investment relative to GDP

- VC investment per capita

- Number of deals per million inhabitants

The results reveal three clear tiers across Latin America: The first tier includes Chile (VEI 40.2), Uruguay (39.1) and Brazil (38.2).

Chile leads the region thanks to the highest VC density per capita at US$12.51 and 2.66 deals per million inhabitants. Uruguay stands out for the highest deal density with 3.53 deals per million people, despite its small population. Brazil combines the highest VC intensity relative to GDP (0.090%) with the largest total investment volume, reaching US$2.032 billion across 363 deals.

The second tier includes Colombia, Mexico, Argentina and Central America, while Peru ranks in the third tier, reflecting a still-developing ecosystem.

Globally, Israel and the United States remain benchmarks, but the report shows that Latin America’s leading ecosystems are approaching the performance levels of other emerging markets such as India.

Larger rounds, fewer deals and a maturing ecosystem

Overall investment data confirms the structural shift in the region’s venture capital market. In 2025, Latin America recorded US$4.126 billion in venture capital investment, while the average round size increased from US$5.2 million to US$6.1 million.

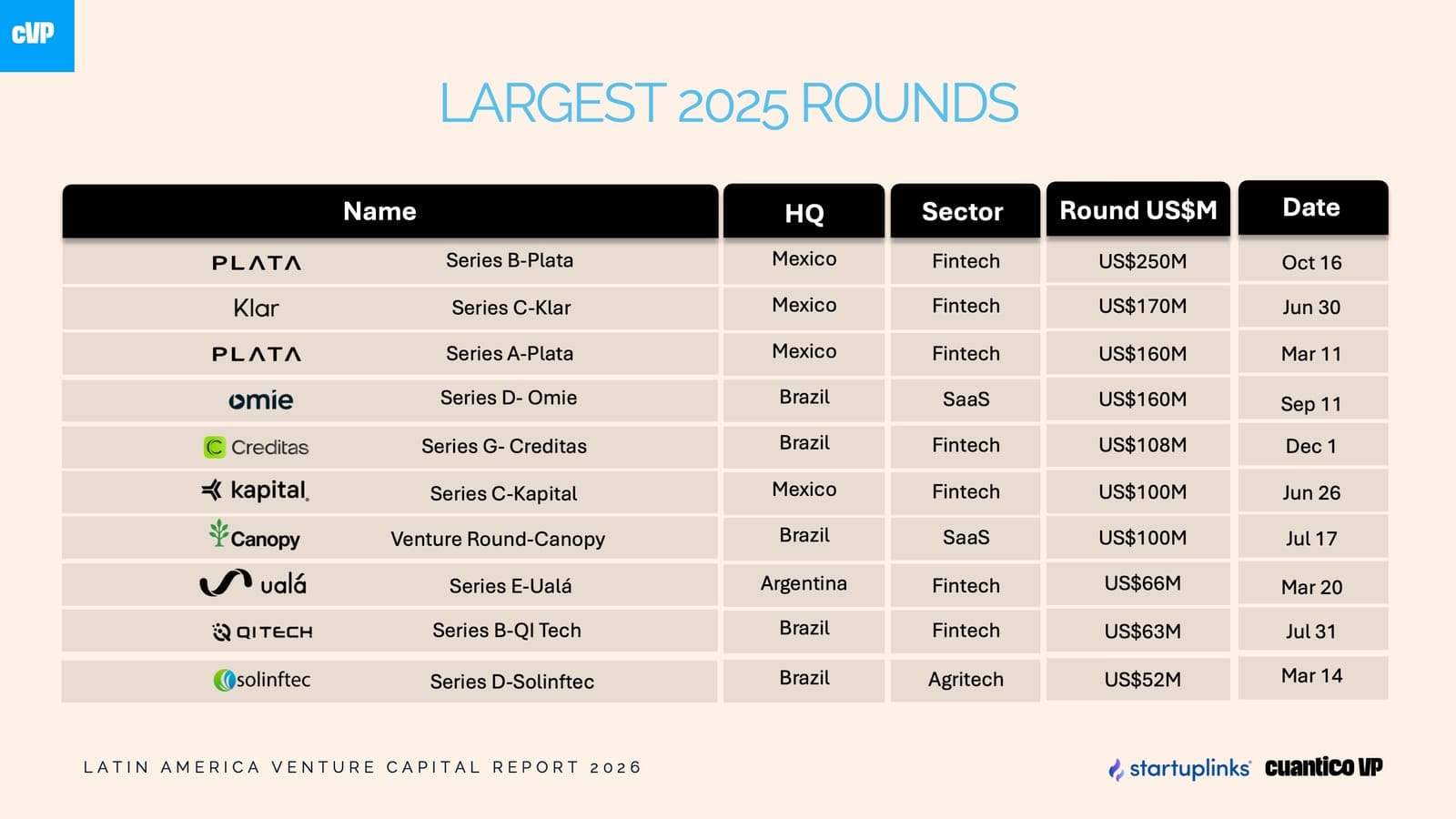

Brazil and Mexico accounted for 78.5% of the total capital deployed, highlighting their central role in the regional ecosystem. Fintech continues to dominate the venture capital landscape, representing 29% of deals and 61% of total capital, driven in part by large rounds raised by companies such as Plata and Klar.

At the same time, pre-seed investment declined sharply, falling 40% in capital and 39.4% in deal count, one of the lowest levels in recent years.

Despite the more demanding environment, 15 new venture capital funds raised US$761 million in 2025, representing 131% growth compared with 2024 and signaling continued confidence from limited partners in the next investment cycle.

“Capital has returned, but it is no longer willing to pay any price or back any company,” said Israel García.

A more disciplined venture capital cycle in Latin America

The Latam VC Report 2026 ultimately portrays a venture capital ecosystem that is becoming more mature and disciplined. The exuberance of 2021 and the contraction between 2022 and 2024 have given way to a new phase characterized by greater selectivity, stronger fundamentals and a clearer focus on returns.

Liquidity is increasingly generated through M&A and secondary transactions, while the next growth cycle is expected to be driven by applied science and deeper technological innovation.

For global investors, the region continues to offer an asymmetric opportunity, combining more rational valuations, increasingly disciplined founders and a persistent gap between perceived risk and long-term potential.

“Latin America is no longer just a trendy narrative — it is a structural thesis for global venture capital,” Kont concluded.