What the 10 Largest VC Rounds in History Are Really Saying

Discover how the 10 largest VC rounds in history are rewriting the global tech landscape, shifting power to AI infrastructure, and creating unprecedented revenue growth.

Over the past three years, we have seen something that had never occurred in the history of venture capital: a single company, OpenAI, raising a US$122B mega-round in 2026, another of US$40B in 2025, and a "non-traditional" US$10B round led by Microsoft in 2023; Anthropic appearing three times in the global top 10 with checks of US$13B, US$30B, and US$65B; xAI, Waymo, Ant Group, and even an enigmatic "Project Prometheus" completing the list.

It is a ranking that looks like a scoreboard from another galaxy, but behind those figures lies something much more important than the shock of the number itself. Each round reveals how the relationship between capital, infrastructure, and technological power is being rewritten on a global scale, and it is precisely there where the following insights converge—insights that almost no one is seeing, revealed in a recent investigation by Cuantico VP, a leading Venture Intelligence firm specializing in emerging markets.

1. SoftBank is building an AI infrastructure monopoly, not just making bets

There is a fundamental difference between betting on who will win a race and building the highway that everyone will have to travel on. Masayoshi Son, the legendary and controversial founder of SoftBank, chose the second option.

SoftBank led or co-led OpenAI's two largest rounds: the $122B one in March 2026 and the US$40B one in March 2025. In total, it committed around $60B to that company alone. SoftBank controls ARM Holdings, the chip designer whose architectures are in practically all mobile devices and increasingly in AI accelerators. Furthermore, it co-founded Stargate, the AI infrastructure project in the United States that committed up to US$500B in datacenters and advanced computing.

What emerges is an unprecedented position: SoftBank has exposure to the most widely used language model in the world (OpenAI), to the chips that process that intelligence (ARM), and to the infrastructure that hosts it (Stargate). If AI becomes the new electricity, SoftBank is building the distribution grid. The question is no longer whether OpenAI will win or lose. The question is: can anyone operate in AI without passing through some SoftBank asset?

2. Anthropic: The Fastest-Growing Company in the History of Private Capital

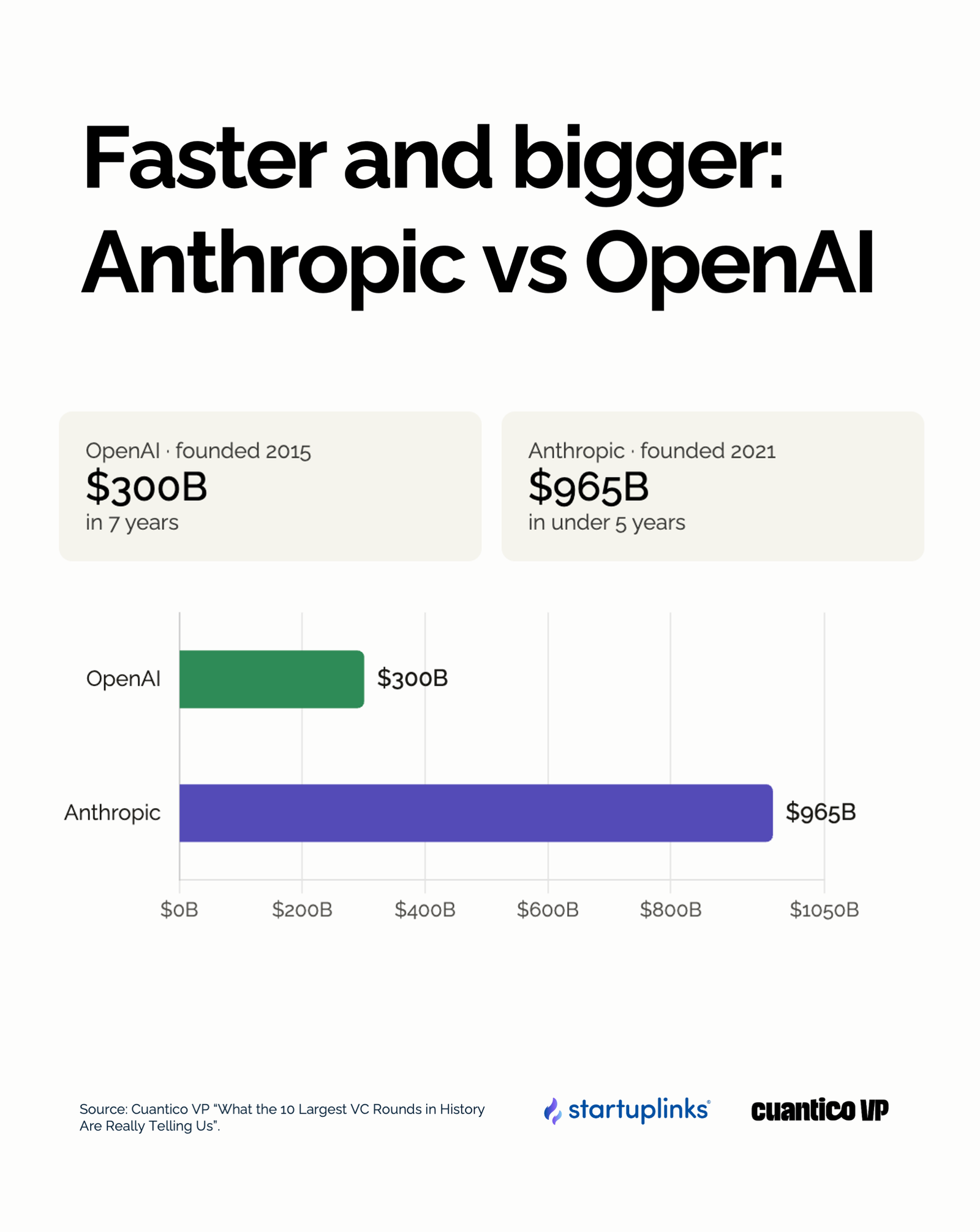

Historical comparisons are difficult to make, but this one is impossible to ignore. OpenAI, founded in 2015, took seven years to reach a valuation of US$300B. Anthropic, founded in 2021, closed its Series H in May 2026 at a valuation of $965B, meaning it reached nearly a trillion dollars in less than five years since its foundation.

Beyond the valuation speed, it is important to look at the revenue speed. At the time of the Series H announcement, Anthropic's CFO revealed that the annualized revenue run-rate had surpassed US$47B. For context: in January 2025, that number was approximately US$1B. In 16 months, Anthropic multiplied its revenue 47X. No technology company has ever done anything similar in that period of time.

With its Series H closed, Anthropic surpassed OpenAI in valuation for the first time, and with an additional detail that many overlooked: the company confidentially filed its S-1 with the SEC just days after the round closed. The largest round in its history could also be its last before its debut in public markets. The clock is already ticking.

3. Capital Is Becoming a Commodity

In January 2023, headlines said that Microsoft had invested US$10B in OpenAI. What those headlines did not explain is that this investment was structurally different from any other on the list. The value did not arrive in cash, but in computing credit: access to Azure servers, scale supercomputing, the ability to train models that would have otherwise cost billions of dollars in proprietary infrastructure.

This was not an accounting whim. It was one of the most massive and notorious examples of an investment model that is becoming a global trend today: Equity for Services. An example of this model is Media For Equity or M4E. In this scheme, investors do not contribute cash capital but rather strategic assets that can be visibility, infrastructure, or audiences, in exchange for an equity stake. What Microsoft did with Azure and OpenAI has a direct conceptual parallel with what specialized Infrastructure or Media investors like MediaForGrowth, Nascent VC, or ILB Media Ventures do.

In a world where building technology is increasingly accessible, scarce assets are distribution, audience, and infrastructure. Whoever controls them has a competitive moat that cannot simply be "funded." Microsoft understood this a few years ago. The rest of the market is understanding it now.

4. The Most Strategic Investor in the Top 10 Is Not from Silicon Valley

When people talk about the big investors in AI, they name Sequoia, a16z, SoftBank, Tiger Global. But there is an actor that appears at least three times in the top 10 VC rounds in history without almost any media outlet pointing it out explicitly: GIC, Singapore's sovereign wealth fund.

GIC co-led Anthropic's US$30B Series G in February 2026 alongside Coatue. It participated in Anthropic's US$13B Series F in September 2025. And it appeared again, once more as a co-lead, in the US$65B Series H in May 2026. Added to its historical participation in Ant Group and other institutional rounds, GIC has quietly become one of the great builders of the global AI ecosystem.

What is relevant here is not just the frequency but the depth. GIC is not diversifying among dozens of small bets. It is concentrating capital in the same companies, round after round, increasing its position as the valuation increases. It is the strategy of an investor that is not looking for quick liquidity, but rather long-term structural influence in the companies that will likely define the digital economy of the coming decades.

5. Project Prometheus: A Mysterious and Important Entry

There is a name on the list that has no recognizable logo, no website, no public product, and barely any media presence: Project Prometheus. With a $10B round in April 2026, it is the only company in the top 10 that is not publicly known nor listed on any market.

It was founded by Jeff Bezos in November 2025, along with Vik Bajaj, a former Google X executive. Its mission, according to Bezos himself, is to create an "artificial general engineer," a radically new tool for designing physical objects, which he described as a "very modern version of CAD" applied to industries like aeronautics, semiconductors, automotive, and pharmaceuticals. It has nothing to do with robotics, he took care to clarify himself, although the confusion was understandable given the profile of its first 120 employees, recruited from OpenAI, DeepMind, Meta, and xAI.

One of the most disruptive insights is not what the company does, but who is financing its growth: BlackRock and JPMorgan appear as anchors of the round. Two traditional financial institutions that historically operate as asset managers or lenders, not as direct investors in Growth VC rounds for early-stage startups. Having major banks enter AI startup rounds as direct co-investors, without going through a VC fund as an intermediary, is a structural break from the traditional venture capital model. And it suggests that Prometheus could be one of the most valuable private companies in the world in the coming years.

6. A Diverse Cap Table is Also a Political Signal

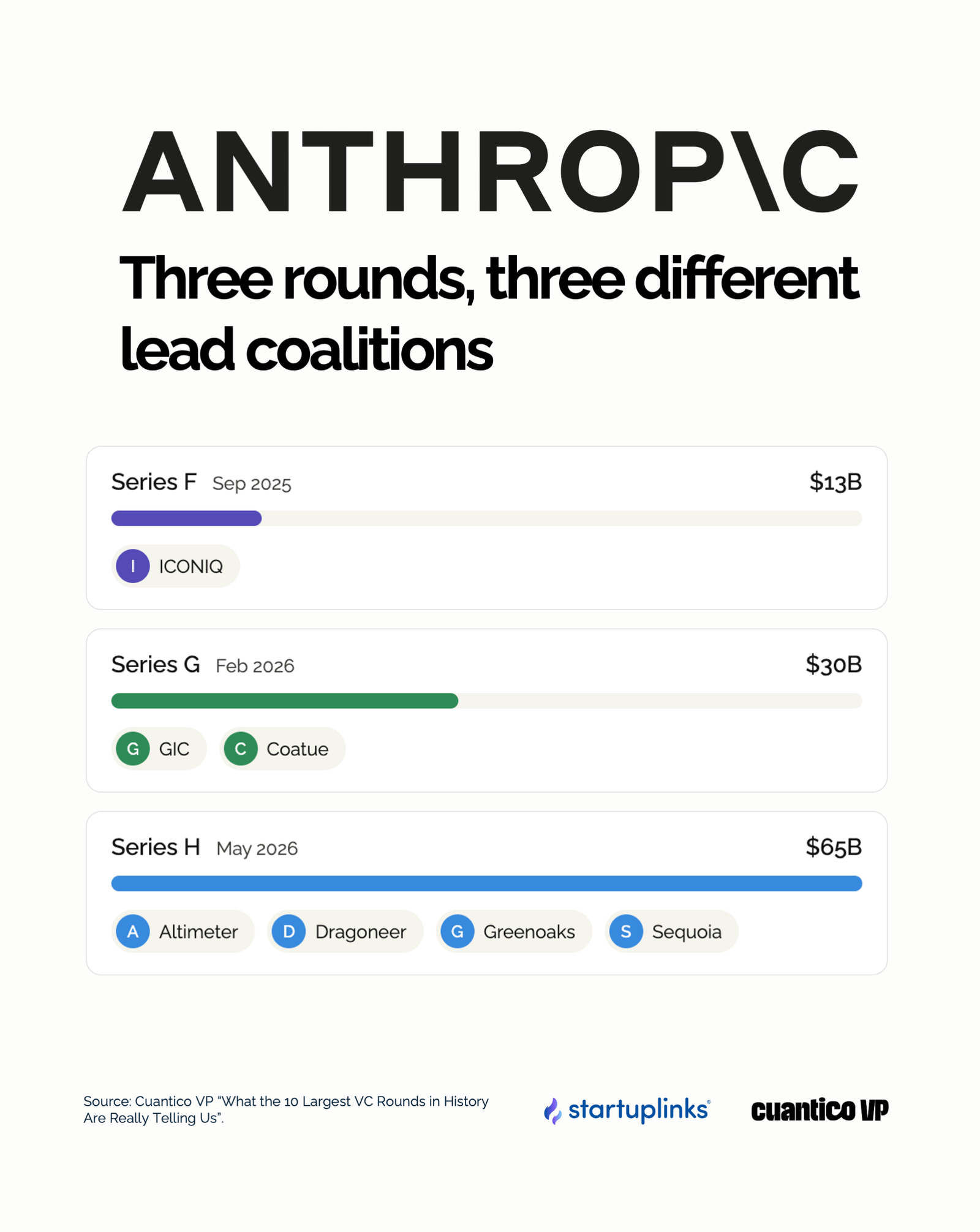

Anthropic appears three times in the top 10. That is striking. But there is something even more revealing: in each of those three rounds, the lead investor was completely different.

Series F (September 2025, US$13B): led by ICONIQ. Series G (February 2026, US$30B): led by GIC and Coatue. Series H (May 2026, US$65B): led by Altimeter, Dragoneer, Greenoaks, and Sequoia. Three rounds. Three different coalitions. Zero repetition in the leadership position.

It is a completely different strategy contrasted with OpenAI, where Microsoft has been the dominant strategic anchor for years and SoftBank has consolidated itself as the most relevant institutional player in the last two rounds. Anthropic, on the other hand, seems to have made a conscious decision not to have a single "godfather." That gives it strategic independence and operational flexibility, but it also means its governance is significantly more complex. When critical decisions arrive, such as the IPO structure, commercial alliances, or acquisitions, there is no single actor who can approve or veto. There is a table with many chairs and voices. For now, that diversity seems like a strength. The question is whether it will remain so when the difficult decisions arrive.

7. The Only Data Point That Proves AI Is Not a Classic Bubble: Revenue

Every time headlines show multi-billion-dollar valuations in companies that have not turned a profit, someone mentions the year 2000. And the comparison makes sense. But there is one data point about the big AI rounds of the past 3 years that completely shatters it: revenue exists, and it is real.

The dot-com bubble was built on promises of future revenue that never arrived, at a time when only 6% of the world's population had internet access. Today, Anthropic revealed in May 2026 an annualized revenue run-rate of US$47B. OpenAI reported approximately US$10B in actual revenue during 2025 and projects reaching US$100B or more in 2026. xAI closed US$20B in its Series E with a valuation close to US$230B, backed by computing infrastructure already deployed.

These are not projections of a hypothetical future. They are current revenues growing at rates that no technology company had ever recorded before in history. The difference between 2000 and 2026 is not one of degree, it is one of nature. So, if it is not a bubble, what is it? It is an accelerated concentration of economic power in a very small number of players. Which, depending on how you look at it, can be more concerning than a bubble.

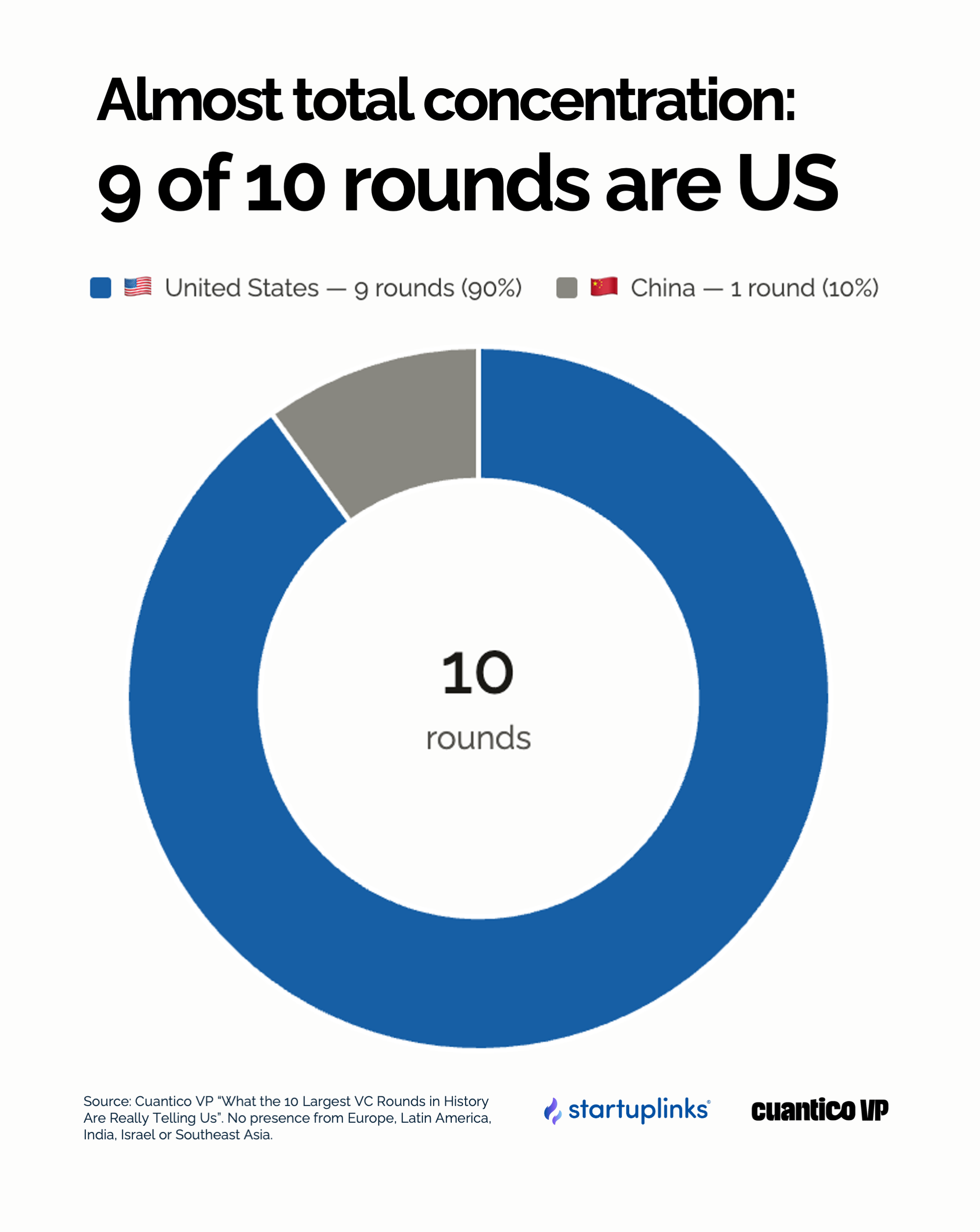

8. Geographical Concentration Is Almost Total: 9 out of 10 Rounds Are US Companies

Of the 10 largest VC rounds in history, 9 correspond to American companies. The only exception is Ant Group, from China, in 2018. There is not a single European company. There is no Latin American one. There are none from India, Israel, or Southeast Asia.

This is not a market accident. It is the result of decades of ecosystem building, capital policies, and talent, and it is now generating a concentration of technological power not seen since the early days of the internet. Something particular about this concentration is seeing where the capital has come from: Middle Eastern sovereign wealth funds like MGX and Qatar Investment Authority, Asian funds like GIC and Temasek, European institutionals like Baillie Gifford. Global capital is flowing into the United States instead of building competitive local ecosystems.

For emerging ecosystems like the Latin American one, the message is clear and urgent: available regional capital is not being deployed in the creation of proprietary AI infrastructure. Every dollar that an Asian or Gulf sovereign wealth fund invests in OpenAI or Anthropic is a dollar that is not building an equivalent in Bogotá, Riyadh, or São Paulo. The concentration is not just technological. It is geopolitical. And by the time local ecosystems want to compete, the gap might already be too large to close quickly.